About six months ago, I penned this piece making the case for Ramaco Resources (METC) as my top pick for this year. In this article, I'll review some key points of interest raised in the first, and expand on recent progress at the company as it continues to develop its business prospects. While there are always positives and negatives in a greenfield project such as this, the net result of the last two reports has been positive, and METC appears to be making solid progress towards its ultimate goal of 4 million tons of production by 2022.

Source

Source

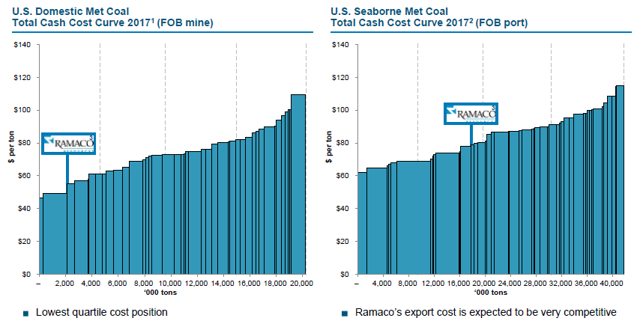

In the first article, I made the case that the most important item for management to achieve would be to validate its claims around costs-per-ton of production. They had made the case that METC should achieve something in the $50 range, which would make them one of the lowest cost producers in the country of met coal. Its fourth-quarter report for the first time gave us what we were looking for, as the company produced a $58.04 cost-per-ton figure.

Unfortunately, the company wasn't able to match that for the first quarter of 2018. Mining for anything is inherently volatile in the prediction field, but greenfield development projects are another level. In this case, METC had issues with its surface mine at Elk Creek. CEO Mike Bauersachs explained the increase this way on the Q1 conference call:

Unfortunately, we faced struggles in the first quarter on the cost and volume front at our Elk Creek surface mine. Simply put, the issues at our surface mine were responsible for the entire increase in our cash cost per ton on a linked quarter basis and overshadow the really good performance by our deep mines. The Elk Creek surface mines faced poor weather, including large amounts of precipitation in the first quarter. We also experienced regulatory delays in obtaining certification for an internal haul road. With that said, the largest issues at our surface mine have been geologic.

We encountered a number of areas that were previously mined. Mostly, these were old auger works, which predated present reporting loss. This unmapped mining was not evident in our advanced planning. These operational challenges increased our mining ratios and decreased the number of days that our high vol miner was able to operate. This negatively impacted our overall production and costs. We've initiated a number of steps to address the surface mine issues. Our current focus is on cost. We've trimmed the workforce and eliminated a second ship to pile on minor production.

For the remainder of this year, we assume our surface mine will have higher mining ratios and that curtailment of high vol miner production will continue. Our cost structure adjustments will take effect in coming quarters. Fortunately, loss surface tons have a high proportion of steam tons in the sales mix. So the decrease in EBITDA is somewhat muted.

Source

Q1's cost-of-production figure came in at $65.02, and management is guiding to slight improvement over the course of the year - i.e., it might take till the end of the year before METC gets back to that $50s figure it produced in Q4 of 2017. While the latest figure is disappointing on a sequential basis, the Q4 report had already provided some validation of the basic thesis around METC's prospects, in terms of its placement in the domestic cost-of-production landscape.

Source: P.13

Coal Quality and Pricing:Clearly, the issue at the surface mine threw a bit of a monkey wrench into the plan for steady progress on the cost front. That's the uncertainty of a development project at play, but sometimes that uncertainty can also lead to upside surprises. On the Q1 '18 conference call, management made the case that its quality of coal production is better than it planned for, and that as initial contracts come up for renewal in the future, it should get better pricing than it initially anticipated. The first question to start off the Q&A section addressed this topic:

Jeremy Sussman

Congrats on posting your first quarterly profit. That's certainly an important milestone for any junior miner transitioning from a developer to a producer. So congrats on that front. I guess one thing I picked up in the prepared remarks, I think you noted that your coal quality has actually been a little bit better than expected. Maybe, can you elaborate on this a bit, sort of what type of mix can we expect towards year end as your low vol Berwind mine ramps up or kind of how should we think about that those comments?

Mike Bauersachs

Yeah. I think on the high vol side, Jeremy, what we've basically found is that, we really don't have a high vol B coal. I mean it is a much better product. Overall, as we've seen now, a great deal history on the mines. So, we expect going forward to have a high vol A and high vol AB product and I think that will translate into higher realizations going forward from what we experienced this year. Without having that experience upfront, it was difficult to place these goals in the marketplace and obviously we placed some of these goals assuming that we would have more or less a high vol B coal plus the other categories. Our low vol coal is actually a very good coal. We expect it to trade at a slight discount for low volatile coals, but believe that especially as we migrate to the number four seam that it is going to be a very strong coal, superior to a lot of the stuff that we see in other Pocahontas 3 seams for example at the mine. So I think that the comment related more or less, Jeremy, to the high vol coals than the low vol coals.

Source

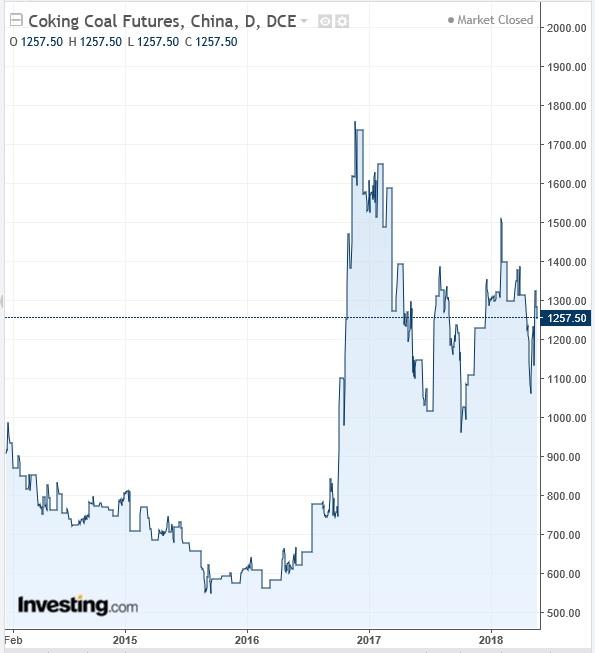

Market Pricing Update:Last time we looked in at the market pricing environment, I showed a chart for coking coal futures prices in China at 1233. Since then the pricing has held up pretty well, and is currently a little bit higher at 1257.

Source

Source

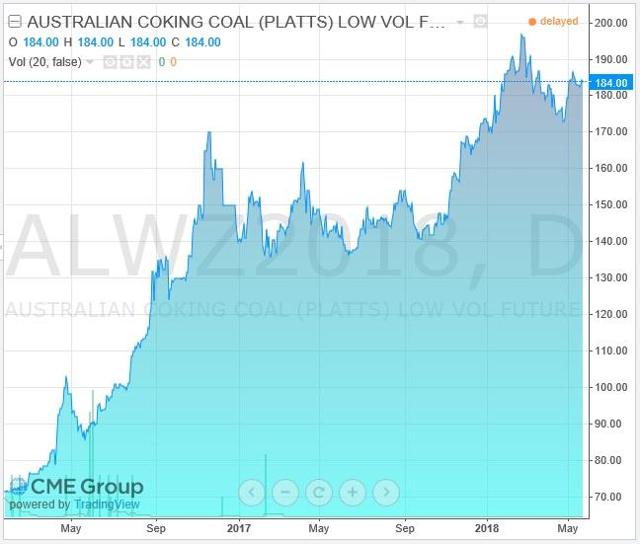

The December futures contract on Australian coking coal that we were looking at has also improved. Increasing from 164 six months ago, to 184 currently.

Source

Source

Thus, market conditions have not only held up, but generally improved to a slight degree. Subsequently, there has been more discussion of met coal pricing holding firmer for longer than the expectation was six months ago.

Model Adjustments:The result of all of the new information we have on my model since the end of last year is the following: my 2018 EPS was .60c, but now is .87c, and my 2018 EBITDA estimate was 39.4 million, but now is 49.8 million. That's good progress. While this stock is really about the total development plan that stretches out to 2022, seeing financial improvement in expectations in the near term is encouraging. It also is significant in the ability for METC to possibly self-finance the future development, without the use of leverage or dilution to current shareholders. That's not a given, and I have no knowledge of its current plans. However, if market conditions continue to improve, then the ability to do so likewise will increase.

One specific modelling issue discussed in my first article on METC was concerned with one Wall Street analyst's estimate for Depletion, Depreciation & Amortization [DD&A]. The analyst had a figure of $37 million, and I made the case for something closer to $9 million. I argued this was likely an error, and due to the few analyst estimates on the street, it was skewing the overall estimate for the stock to the downside. Q1's DD&A figure came in at $2.4 million. Hence, now I'm using a $10 million estimate for this year. That's higher than my initial estimate, but clearly nowhere near that $37 million figure.

Conclusion:METC is making good progress. There's some give and take as should be expected in a development project, but the net result is progressing nicely. The market is continuing to be accommodative with good pricing while METC builds out its production capacity. The price of the stock has been reflecting these improvements. When I started writing the first article in December of '17, METC had a $4 handle on it. By the time I finished the article, it was trading at about $5.40. Now as I finish this review, it's trading at $7.63.

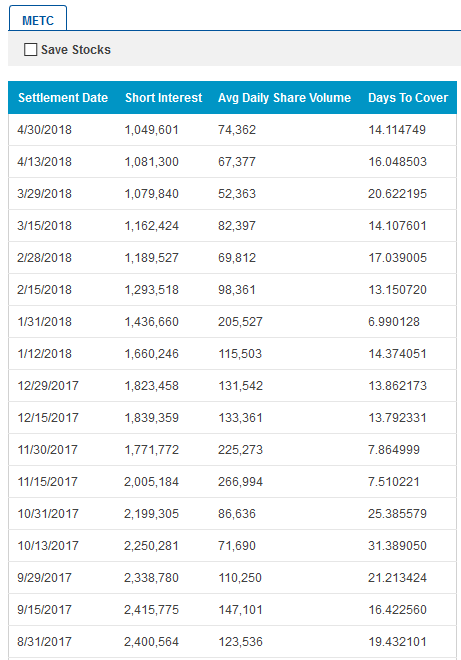

Part of the improvement in the stock's pricing has come from a source that I expected could get caught wrong-footed. At that time we knew that there were about 1.77 million shares short the stock with an approximate 6 million float in the market. In other words, about 30% of the trading float of METC was short the stock at the time. Since then we've seen a decent decline in the short interest of the stock to just over 1 million shares. That's still nearly 17% of the float.

Source

Source

Finally, I also mentioned the possibility of dividend payments this year as the company began to produce enough excess free cash flow to warrant some returns to shareholders. That still looks to be the case, but it appears investors may have to wait until the end of the year. Management bumped up its expected Capital Expenditures for 2018 in response to the weather and train delay issues it managed through in Q1. The result is more of the free cash flow this year is getting diverted to improving the access to market for production. The question was addressed on the recent conference call, and here's how management responded:

Jeremy Sussman

Maybe shifting, just maybe a little bit early to be bringing this up, but given you just posted your first profit, I know going back to sort of the beginnings of Ramaco, you had noted that sort of the medium to long term capital return strategy was to pay out dividends from free cash flow. I guess as the year progresses and earnings ramp up, ultimately, is there any change to that? I guess, how should we think about how you are thinking about kind of returning cash to shareholders down the road?

Randy Atkins

I think, Jeremy, this is Randy, I think as we've said all along, we're going to review that towards the latter part of the year, sort of see where we are in terms of cash generation and make a decision at that time. Basically, our uses for capital are either to use it in the business or return it back to our shareholders. So, that comment that we made earlier has not changed and I would say probably sometime in to the early part of the fourth quarter, we will be making a call on that.

Source

Bottom line, there still is plenty of work to be done by METC between here and 2022, but so far we've seen good progress to date and the stock price has rewarded investors. Good luck to everyone out there.

Disclosure: I am/we are long METC.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

No comments:

Post a Comment